Electronic Components Industry

2024 Results, 2025 Outlook, and Supply Chain/Innovation Metrics

Research Report for kunkune.co.uk

Published: August 2025

Executive Summary

Key Takeaways

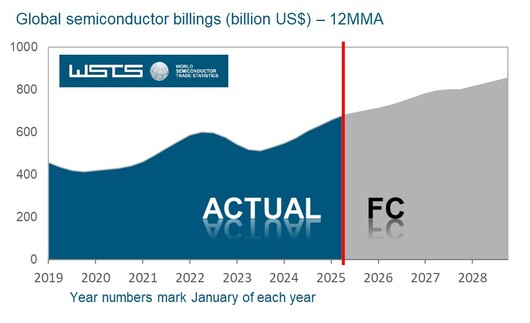

- • Global semiconductor sales rebounded to $630.5B in 2024 (+19.1% YoY)

- • WSTS forecasts $700.9B in 2025 (+11.2%) driven by logic and memory

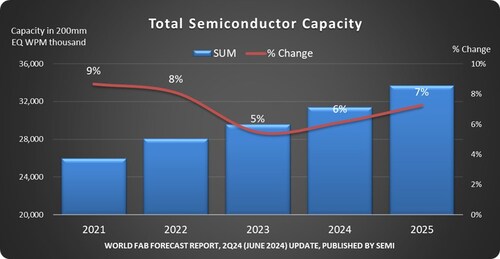

- • Fab capacity expanding 6% in 2024, 7% in 2025 to record 33.7M wafers/month

- • Supply chain pressures re-emerging: Lead time index hit record 166.6 in April 2025

- • EV market continues growth: 17M units expected in 2024 (>20% share)

The global electronic components industry demonstrated remarkable resilience in 2024, with semiconductor sales reaching an updated record of $630.5 billion, representing a 19.1% year-over-year increase from $526.8 billion in 2023. [Semiconductor Industry Association]

Regional performance varied significantly, with the Americas leading growth at +44.8%, followed by China (+18.3%) and Asia Pacific/All Others (+12.5%), while Japan (-0.4%) and Europe (-8.1%) experienced contractions. The World Semiconductor Trade Statistics (WSTS) projects continued momentum into 2025, forecasting $700.9 billion in sales (+11.2%). [WSTS]

Semiconductor Market Statistics

2024 Performance

- • Global sales: $630.5B (+19.1% YoY)

- • Q4 2024: $170.9B (+17.1% YoY)

- • Q3 2024: $166.0B (+23.2% YoY)

- • Dec 2024: $57.0B (-1.2% MoM)

2025 Outlook

- • Forecast: $700.9B (+11.2%)

- • Logic: Double-digit growth

- • Memory: Double-digit growth

- • Discretes: Low single-digit decline

Regional Performance 2024

| Region | YoY Growth | Performance |

|---|---|---|

| Americas | +44.8% | Strong AI/Data Center Demand |

| China | +18.3% | Domestic Production Ramp |

| APAC/Others | +12.5% | Manufacturing Recovery |

| Japan | -0.4% | Mature Market Challenges |

| Europe | -8.1% | Auto/Industrial Softness |

Fab Capacity & Equipment Investment

Capacity Expansion Highlights

Overall Growth

- • 2024: +6% to 31.7M wpm

- • 2025: +7% to 33.7M wpm

- • Leading-edge (≤5nm): +13% (2024), +17% (2025)

By Segment

- • Foundry: +11% (2024), +10% (2025)

- • DRAM: +9% both years

- • 3D NAND: 0% (2024), +5% (2025)

Equipment Sales Forecast

$125.5B

Total Equipment 2025

+7.4% YoY

$110.8B

WFE 2025

+6.2% YoY

$138.1B

Total Equipment 2026

+10.0% YoY

Sources: [SEMI via PR Newswire], [SEMI]

Memory Bit-Demand Recovery

DRAM Market

- • 2024 bit demand: +13% YoY

- • Equipment spending: +40.2% in 2024

- • HBM driving capacity investments

- • AI training/inference demand

NAND Flash Market

- • 2024 bit demand: +16% YoY

- • Equipment spending: +4.1% in 2024

- • 3D NAND stacking advances

- • Slow recovery from 2023 lows

After a challenging 2023 that established a low baseline, the memory sector experienced significant recovery in 2024. TrendForce anticipates year-over-year bit demand growth rates of 13% for DRAM and 16% for NAND Flash, driven by current low pricing for memory products and inventory restocking. [TrendForce]

Memory Technology Trends

- • HBM Adoption: Exploding AI adoption drives investment in high bandwidth memory

- • 3D NAND Evolution: Capacity expansion supporting advanced stacking technology

- • Process Migration: Leading manufacturers transitioning to next-gen nodes

- • Supply Discipline: Improved capacity utilization following inventory corrections

Passive Components Market

MLCC (Multilayer Ceramic Capacitors)

Global Market Size

4.193 Trillion

MLCC units demanded in 2023

+3% YoY growth

Murata Market Position

~40%

Global MLCC market share

Ships >1 trillion units/year

Supplier Concentration Risk

The MLCC market demonstrates significant supplier concentration, with Murata commanding an estimated 40% global market share and shipping over 1 trillion units annually. This concentration creates potential supply chain vulnerabilities.

Market Drivers

- • Automotive electronics

- • 5G infrastructure

- • Industrial automation

- • Consumer devices

Supply Challenges

- • High barrier to entry

- • Technology concentration

- • Capacity constraints

- • Raw material dependencies

Sources: [TrendForce], [Murata Value Report 2024]

Sensors & IoT Components

MEMS Market Recovery

$15.4B

2024 Revenue

+5%

YoY Growth

31B units shipped in 2024

2030 forecast: $19.2B

IoT Device Growth

18.8B

Connected Devices 2024

+13%

YoY Growth

2023: 16.6B devices

2030 forecast: ~40B devices

Sources: [Yole Group], [IoT Analytics]

PCB Industry Recovery

Global Market Estimates

-

Prismark (via TTM 10-K): $73.6B

-

iConnect007 estimate: $78.2B+6.3% YoY growth

Regional Production Share

- • China: ~56% (~$41.0B)

- • Rest of World: ~39% (~$29.2B)

- • Americas: ~5% (~$3.4B)

North American PCB Performance

April 2024 Performance:

Shipments: +9.4% YoY

Month-over-Month: +18.6%

Bookings: +2.6% YoY

Month-over-Month: +2.9%

PCB Market Drivers

Growth Catalysts

- • AI/Data center demand

- • 5G infrastructure

- • Electric vehicle adoption

- • Industrial automation

Technology Trends

- • Higher layer counts

- • Advanced packaging

- • Flexible/rigid-flex

- • Embedded components

Sources: [TTM Technologies 10-K citing Prismark], [iConnect007], [EPP Europe News]

Automotive & EV Markets

92.5M

Global Vehicle Production 2024

-1% YoY

17M

EV Sales 2024 (Forecast)

~20% market share

$67B

Auto Semiconductors 2023

+12% YoY

Top Vehicle Producing Countries (2024)

| Country | Production (M units) | YoY Change |

|---|---|---|

| China | 31.28 | +4% |

| USA | 10.56 | -1% |

| Japan | 8.23 | -9% |

| India | 6.01 | +3% |

| Mexico | 4.20 | +5% |

| Germany | 4.07 | -1% |

EV Market Momentum

Global Growth

- • 2023: 14M units (18% share)

- • 2024F: 17M units (>20% share)

- • 35% YoY growth in 2023

Regional Outlook 2024

- • China: ~45% EV share

- • Europe: ~25% EV share

- • USA: >11% EV share

Semiconductor Impact

- • Power electronics demand

- • MCU/sensor growth

- • Battery management ICs

Sources: [OICA], [Semiconductor Intelligence], [IEA Global EV Outlook 2024]

Trade & Supplier Concentration

Integrated Circuits Trade (HS 8542) – 2023

Global Trade Volume

Market Concentration

• Top 5 importers: 82.2% of trade

• Top 5 exporters: 80.4% of trade

• Asian hubs dominate flows

Top IC Importers 2023

Top IC Exporters 2023

Supply Chain Risk Assessment

The concentration of IC trade in a few Asian hubs creates systemic risks. Hong Kong and China combined account for ~58% of IC exports, while China alone represents 38% of global imports.

Risk Factors

- • Geopolitical tensions

- • Trade policy changes

- • Logistics bottlenecks

- • Natural disasters

Mitigation Strategies

- • Supply chain diversification

- • Strategic inventory

- • Alternative sourcing

- • Nearshoring initiatives

Source: [TrendEconomy]

Supply Chain Indicators

Lead Time Alert: 2025 Surge

Supply chain pressures have returned with unprecedented intensity in 2025, surpassing even the pandemic-era disruptions.

Current Status

- • Supplyframe Index: 166.6 (Apr 2025)

- • Previous record: 146.7 (Jan 2022)

- • 85% increase Mar→Apr 2025

- • Capacitors: +43% lead time spike

Key Drivers

- • Trade policy uncertainties

- • AI infrastructure demand

- • Inventory destocking

- • Supplier diversification efforts

Lead Time Evolution

25.8 weeks

Peak Lead Time

Q4 2021 (Susquehanna)

~24 weeks

Improved Level

Dec 2022 (-8 days MoM)

166.6

Lead Time Index

Apr 2025 (Record High)

Industry Sentiment

ECIA ECST Survey (June 2024)

Component Index: 98.9 (-13.4 points MoM)

Cumulative decline: -25 points (May-June)

Below 100 = contraction

July Outlook: 111.9 (expected)

Improvement: +13 points

Cautious optimism

Sources: [Astute Group], [Pasadena Now], [Supply & Demand Chain Executive], [ECIA]

Innovation & R&D Investment

U.S. R&D Leadership

Investment Scale

Industry Ranking

• 2nd highest R&D intensity among U.S. industries

• Only behind pharma/biotech sector

• Sustained >15% rate for 20+ years

• Drives global technology leadership

$62.7B

U.S. Semiconductor R&D

2024 (+5.7% YoY)

17.7%

R&D/Revenue Ratio

2nd highest U.S. industry

20+

Years >15% R&D Rate

Sustained innovation

R&D Focus Areas

Technology Priorities

- • Advanced process nodes (3nm, 2nm)

- • AI/ML accelerator architectures

- • Quantum computing development

- • Advanced packaging solutions

- • Power efficiency innovations

Strategic Investments

- • Materials science research

- • EUV lithography advancement

- • Chiplet/heterogeneous integration

- • Neuromorphic computing

- • Sustainability technologies

Source: [Semiconductor Industry Association – State of the Industry 2025]

Statistical Appendix

Key Market Indicators

Supply Chain Metrics

Data Sources

• Semiconductor Industry Association (SIA) – Global sales data and regional breakdowns

• World Semiconductor Trade Statistics (WSTS) – Market forecasts and segment analysis

• SEMI – Fab capacity projections and equipment sales forecasts

• TrendForce – Memory bit-demand and MLCC market sizing

• Yole Group – MEMS market analysis and unit shipments

• IoT Analytics – Connected device projections and growth rates

• OICA – Global vehicle production statistics

• IEA – Electric vehicle market analysis and regional forecasts

• TrendEconomy – Integrated circuit trade flow data

• Supplyframe/Susquehanna – Lead time indicators and supply chain metrics

• ECIA – Electronic component sales trends and sentiment

• Various industry sources – PCB market estimates and regional data

Report Methodology: This analysis combines data from authoritative industry sources, regulatory filings, and market research organizations. All statistics include inline citations to enable verification and deeper research. Market estimates may vary between sources due to different methodologies and scope definitions.